Iceland and the EU: What Membership would mean for the average Icelander

The Question Before Iceland

On 29 August 2026, Icelanders will vote on whether to resume European Union accession negotiations. The ballot asks a narrow question: not whether to join, but whether to reopen the talks that collapsed in 2013. If voters say yes and those talks eventually conclude, a second referendum would follow on actual membership.

The polls, as of early 2026, show the country split evenly: 42% in favour, 42% opposed, 16% undecided. That final group will settle the matter. This assessment is written for them.

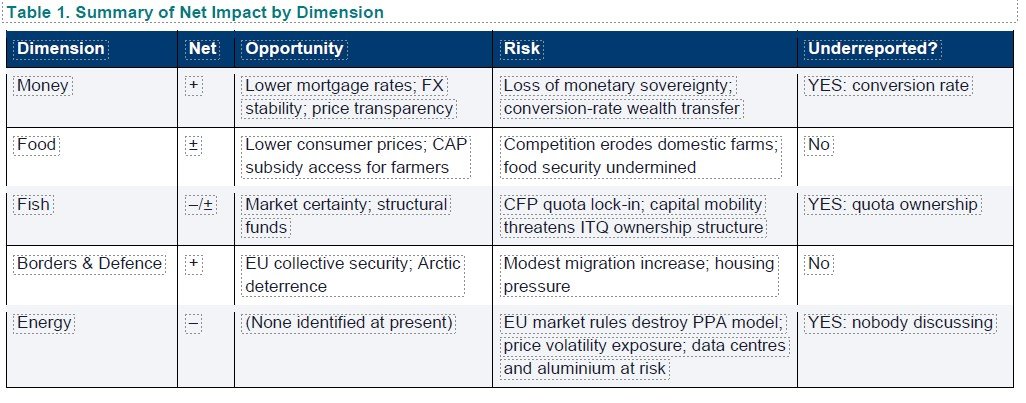

1. Money

What is not being discussed? First, the conversion rate. When the króna is retired, every mortgage, pension balance, and savings account will be converted to euros at a rate fixed by the EU Council under TFEU Article 140(3). Iceland will have a voice but not a veto. The rate chosen determines a one-time, irreversible wealth transfer between savers and borrowers, potentially amounting to billions.

Iceland's GDP per capita is approximately USD 91,000, fifth highest globally. By that measure, Iceland is one of the most successful small economies in the world. But the headline number conceals a persistent cost-of-living problem rooted in the nature of the currency itself.

The króna serves a population smaller than that of Coventry. It is volatile, illiquid, and essentially untradeable outside Iceland. The Central Bank ended 2024 with a policy rate of 8.50%, and inflation was still running at roughly 4% in early 2025, almost double the 2.5% target. Icelandic households carry mortgage costs that their Scandinavian neighbours would find remarkable.

EU membership would, in time, require euro adoption. There is no opt-out available to new member states; TFEU Article 140 makes this explicit, and Denmark's exemption under Protocol 16 was negotiated before Maastricht and cannot be replicated.4 For the average household, the consequences would be felt quickly. ECB policy rates have been structurally lower than Iceland's for most of the past fifteen years. A reduction of 200 to 300 basis points on a typical Icelandic mortgage would translate into savings of several hundred thousand krónur a year. One academic study estimated that euro adoption could increase Icelandic international trade by up to 60%, simply by removing the friction the króna imposes on every cross-border transaction.

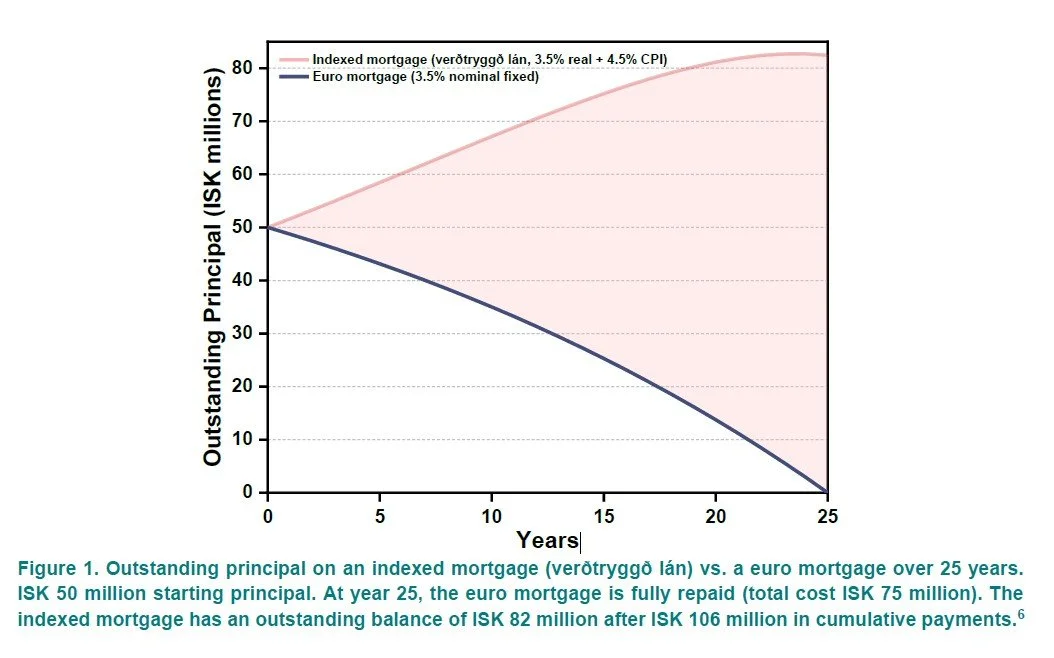

The interest rate differential is only half the story. Most Icelandic mortgages are inflation-indexed (verðtryggð lán), a system introduced in 1979 to combat hyperinflation and never removed. The outstanding principal adjusts monthly by the Consumer Price Index. With CPI running at 4 to 6%, the amount owed on a home increases every month even as payments are made. A household that borrowed ISK 50 million at a 3.5% real rate with 4.5% average inflation sees its nominal principal rise above ISK 60 million within four years, despite making every scheduled payment. Euro-denominated mortgages do not work this way. No eurozone country uses CPI-indexed principal on residential loans.

Euro adoption would not merely reduce the rate; it would eliminate indexation entirely. The difference over the life of a loan is substantial. After 25 years of payments on a euro mortgage at 3.5% fixed, the household has paid ISK 75 million and the loan is fully discharged. After the same 25 years on an indexed mortgage, the household has paid ISK 106 million and the outstanding principal stands at ISK 82 million, exceeding the original loan amount. The indexed mortgage has a further fifteen years of payments remaining.

The housing crisis sits underneath the mortgage question. Iceland’s Housing and Construction Authority estimates current construction meets only 56% of projected need. Average house prices in the capital region reached ISK 87 million (roughly USD 620,000) in early 2025, rising at over 11% annually. EU membership would reduce imported construction material costs through full single market access and expand the labour supply the sector demonstrably needs. The constraint it would not solve is land supply: Reykjavík’s geography limits buildable land regardless of EU rules. And if euro adoption reduces mortgage costs before construction supply catches up, the result is a demand surge into a supply-constrained market.

Iceland already operates as a de facto euro-adjacent economy. Import and export invoicing is denominated in euros or US dollars, not krónur. Large borrowing is frequently FX-linked. The Central Bank tracks ECB decisions with a structural premium reflecting the króna’s risk characteristics rather than any fundamental monetary divergence. The króna functions less as a sovereign instrument and more as a friction layer: adding transaction costs, exchange rate risk, and a volatility premium to every cross-border interaction without providing the adjustment capacity its defenders claim. Euro adoption would formalise what already exists while removing the costs of maintaining the fiction of monetary independence.

The counterargument deserves serious treatment. The króna's ability to devalue acted as a genuine shock absorber during the 2008 banking collapse. Exports became cheaper, tourism surged, and Iceland recovered faster than several eurozone countries locked into a currency they could not adjust. The ECB sets rates for 350 million people, and Iceland's business cycle will not always coincide with that of Germany or France. Set against that: the OECD has repeatedly found that Icelandic monetary and fiscal policy has been pro-cyclical, amplifying booms and deepening busts rather han smoothing either. The instrument being surrendered has not, in practice, been used as well as its defenders suggest.

But the strongest counterargument is not about the króna as shock absorber. It is about what happens when the shock absorber is removed and nothing replaces it. Euro adoption means Iceland cannot devalue, cannot print, and cannot set its own rates. The 2008 crisis inside the eurozone would have meant not a 50% króna devaluation that restored competitiveness within two years, but the path taken by Greece, Ireland, and Portugal: internal devaluation through wage cuts, austerity, and sustained unemployment. Iceland’s government debt-to-GDP hit 136% after the collapse; that figure would have triggered a sovereign debt spiral. The króna’s collapse was brutal for households. It was also the mechanism through which the economy corrected.

The question for undecided voters is not whether GDP goes up. It is whether the money left in their account at the end of the month goes up. Iceland has the fifth-highest GDP per capita, high nominal salaries, and household debt at 71% of GDP. What matters is the residual: income minus housing, minus debt service, minus groceries. Euro adoption would compress debt service substantially and likely reduce consumer prices, but it would also remove the currency channel through which wages have historically adjusted. Every eurozone member that has faced an asymmetric shock since 2008 has experienced wage compression, public sector cuts, or elevated unemployment. Whether sustained cost reductions outweigh periodic but severe adjustment costs depends on the frequency of future shocks. The honest answer: nobody knows.

The conversion rate is not an abstraction. It sets the euro price of every Icelandic house, every mortgage, every pension, every fishing quota, and every export. If the króna converts too high, Icelandic assets become expensive overnight: houses overvalued, tourism uncompetitive, wages unaffordable relative to productivity. If it converts too low, every asset in a country of 400,000 becomes cheap in euro terms, inviting a capital inflow the market cannot absorb. The króna has fluctuated by more than 30% against the euro in the past decade. There is no obviously correct rate, only a range of defensible ones, each with different winners and losers.

Two precedents illustrate what happens when this goes wrong. The Ostmark-Deutsche Mark conversion of 1990 was set at a politically irresistible 1:1 against a market rate closer to 4:1. The result was mass unemployment across the former East. Greece in 2015 demonstrated the opposite failure: a technically coherent negotiating position that never engaged with what the creditor bloc needed in order to say yes, and consequently lost the room. One was idealistic politics overriding economics. The other was economics that never learned to play the politics.

Iceland will have one voice and no veto. TFEU Article 140(3) gives the EU Council the final decision. The outcome will not be determined by which rate is economically optimal. It will be determined by whether Iceland fields a negotiating team that understands the institutional incentives of the Commission, the Council, and the ECB, and can construct a proposal the counterparties can accept without setting a precedent they cannot live with. That team does not yet exist. Building it should start now.

The króna protects the macroeconomy through devaluation but punishes households through inflation, indexed mortgage growth, and exchange-rate instability. The euro would protect households through stable prices, lower borrowing costs, and elimination of indexation, but would constrain the macroeconomy by removing the devaluation option. The question is not which system is better in the abstract. It is whether Iceland can negotiate the transition terms (convergence criteria, conversion rate, timetable) in a way that captures the household benefits while building fiscal buffers against the macroeconomic constraints. That requires a negotiating position developed before the talks begin, not improvised during them.

2.Food

Net assessment: the average household’s grocery bill would fall. That matters in one of Europe’s most expensive food markets, but the transition will not manage itself. Every accession negotiation includes adaptation periods for agriculture, and Iceland’s negotiators will need to know precisely what they are asking for: which product categories require extended tariff protection, which rural communities qualify for Pillar II investment, and how to structure the CAP application so that funds flow to the small farms that need them rather than the large operations that will capture them by default. The Finnish and Austrian accession negotiations of 1994 provide templates. Iceland should be studying them now.

Agriculture contributes roughly 3.9% of GDP and meets approximately half of Iceland's food requirements.8 The sector is built on sheep and cattle farming, supplemented by greenhouse horticulture that uses geothermal heat to grow tomatoes and cucumbers at latitudes. A government food policy adopted in 2023 targets greater domestic self-sufficiency through 2040.9

The policy framework is protectionist in a way that EU membership would not permit. Import tariffs on competing agricultural products are high. Domestic subsidies are structured through ten-year agreements between the government and the Farmers' Association. Phytosanitary regulations differ from EU standards. The result is that food prices in Iceland sit well above even Norway and Denmark. Every trip to Bónus or Krónan includes a premium for the privilege of domestic production.

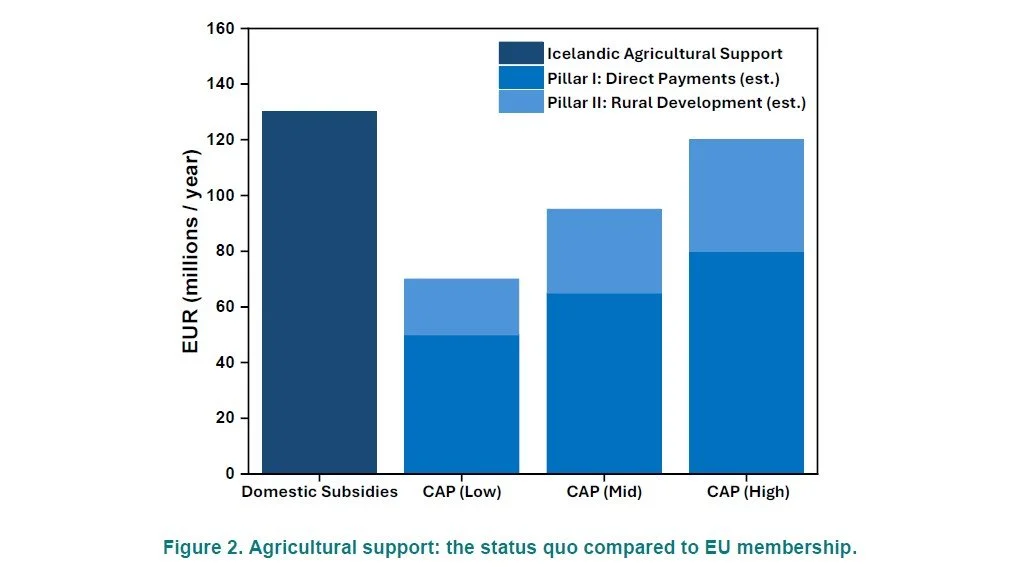

EU accession would require alignment with the Common Agricultural Policy, including direct payment schemes, rural development programmes, and the regulatory infrastructure of the single market in food products. Consumer prices would fall, particularly on dairy, grain products, and imported processed foods. Icelandic farmers would gain eligibility for CAP funds; the 2023 to 2027 CAP budget exceeds EUR 380 billion, and even a modest share applied to fewer than 4,000 farms could make a material difference.

The risk sits on the other side of the ledger. CAP integration could make it cheaper to import than to produce locally, particularly for beef and dairy where Icelandic unit costs are structurally high. Rural farming communities, already under demographic pressure, would face competition from continental producers operating at scales that Iceland cannot match. The cultural weight of Icelandic agriculture exceeds its GDP contribution, and that is not something a subsidy from Brussels can fully replace.

The risk to rural communities is concrete, not abstract. A village that loses its dairy farm does not just lose farm jobs. It loses the mechanic who services the equipment, the teacher whose salary the school justifies only because farm families have children enrolled, the cooperative store whose turnover depends on the farming population. When the farm goes, the services follow. This is the documented pattern across rural Ireland, Scotland, and Finland after integration with EU agricultural markets. CAP Pillar II rural development funds could partially offset this, but accessing them requires administrative capacity that small Icelandic municipalities may not possess. Brussels can write the cheques. It cannot keep the school open.

A further consideration: Icelandic consumers display strong preference for domestic lamb, dairy, and greenhouse vegetables. Imported alternatives that undercut on price will not automatically displace local products where cultural attachment sustains demand. The likely result is a two-tier food economy: prices would fall on the products that face direct competition from imports: processed foods, grain products, generic dairy. They would hold steady on the products Icelanders prefer to buy Icelandic: lamb, skyr, greenhouse vegetables. The average grocery bill gets lighter, but not evenly.

Quantifying likely CAP receipts requires assumptions, but the order of magnitude is instructive. Iceland has approximately 3,800 farms and 1.9 million hectares of agricultural land, mostly rough grazing. Under the 2023–2027 CAP framework, direct payments averaged approximately EUR 267 per hectare across the EU. Even at half the average rate on actively farmed hectares, Pillar I payments could reach EUR 50 to 80 million annually, with Pillar II adding EUR 20 to 40 million. For context, Iceland’s current agricultural subsidies total approximately EUR 130 million per year. CAP participation would shift part of this base from the Icelandic taxpayer to the EU budget, resulting in significant saving for Icelandic taxpayers. The final amount even be higher, depending on the outcome of negotiations.

3.Fish

If the referendum produces a mandate to negotiate, the fisheries chapter must be opened at the start of the process, not the end. The 2010 to 2013 talks collapsed not because of an abstract sovereignty dispute but because a bilateral mackerel conflict gave Ireland and the UK veto power over the fisheries chapter. A member of the European Parliament’s fisheries committee whose family owned one of Ireland’s largest mackerel export firms led a campaign to ban all Icelandic seafood imports into the EU. Iceland was saved from a trade war only by the personal intervention of the Swedish and German foreign ministers. The enlargement commissioner, Stefan Füle, was too weak within the institution to overrule the blocking coalition. These are the dynamics that determine outcomes: not legal positions but bilateral relationships, committee politics, and an understanding of who on the other side has something to lose.

Every serious discussion of Iceland and the EU arrives at this point. Fisheries account for approximately 40% of merchandise export earnings, over 12% of GDP through the broader ocean cluster, and up to a fifth of total employment. Iceland is the second-largest fishing nation in the North-East Atlantic. Its Individual Transferable Quota system is internationally recognised as one of the most effective models of sustainable fisheries management in operation.

The emotional weight is at least as important as the economic data. The Cod Wars of 1958 to 1976, in which Iceland successfully faced down the Royal Navy to establish its exclusive economic zone, are the origin story of modern Icelandic sovereignty. Control over marine resources is not a negotiable economic preference. For a large part of the electorate, it is a constitutional instinct.

The legal architecture is unambiguous. The CFP is an exclusive competence of the Union under TFEU Article 3(1)(d). Upon accession, Iceland would transfer authority over conservation, quota-setting, and fleet access to EU institutions. The 'relative stability' principle in Regulation 1380/2013, Article 16(1), allocates quotas between member states on the basis of historical catch patterns. No permanent derogation from the CFP has ever been granted to any member state.

The Irish Precedent

Ireland, which joined the EEC in 1973, provides the closest available comparison. Its Atlantic waters became part of the common fishing area. Ireland retained exclusive access within six nautical miles, and largely within twelve, but the deeper offshore grounds were opened to fleets from other member states under CFP quota management. The relative stability formula locked in allocations reflecting the capacity of the Irish fleet in the early 1970s, not the productivity of Irish waters. Fifty years later, Irish fishing organisations are still contesting those allocations.

The difference that matters: fishing was roughly 1% of Ireland's GDP at the time of accession. It is north of 12% of Iceland's. What has been a persistent regional grievance in Galway and Killybegs would, at Icelandic scale, constitute a national economic restructuring. The formula agreed at the moment of entry will define who catches Icelandic fish for decades. Ireland's experience demonstrates that these baselines, once set, prove extraordinarily difficult to renegotiate.

The Angle Nobody Is Discussing: Quota Ownership and EU Competition Law

The conventional fisheries debate is framed in terms of foreign boats entering Icelandic waters. That framing is incomplete. There is a second, less visible threat to the current structure of Iceland's fishing industry, and it runs through EU competition law and the free movement of capital rather than through the Common Fisheries Policy directly.

Iceland's ITQ system, introduced in the 1980s and made full under the Fisheries Management Act 1990, allocates permanent, tradeable quota shares based on historical catch records.15 Over three decades, quota consolidation has concentrated fishing rights in the hands of a small number of families and companies. The system is domestically controversial: the Icelandic constitution states that marine resources are the common property of the nation, and the UN Human Rights Committee has ruled that the quota allocation system violated the non-discrimination principle of the International Covenant on Civil and Political Rights.

EU membership would subject this system to two legal pressures that the domestic debate has not yet confronted. First, TFEU Article 49 (right of establishment) and Article 63 (free movement of capital) would, in principle, require Iceland to allow EU-based companies and investment funds to acquire Icelandic fishing quotas through purchasing the companies that hold them.17 Currently, non-Icelandic ownership of fishing entities is capped at 25% of share capital. These restrictions would need to be renegotiated or eliminated. The prospect of Danish, Spanish, or Dutch-owned companies legally acquiring the right to harvest Icelandic fish by buying quota-holding firms is the scenario that would cause genuine upheaval.

Second, the ITQ system's allocation of permanent economic advantages to incumbent holders, at the expense of new entrants (including entrants from other member states who would have the right of establishment in Iceland), is potentially incompatible with EU state aid rules and competition law. The current quota holders have every incentive to keep this discussion suppressed, because the existing system serves them perfectly: they control a permanently allocated resource base that cannot be purchased by outsiders. EU membership threatens that control not through foreign boats in Icelandic waters but through foreign capital in Icelandic boardrooms.

The political dynamics here are worth noting. The quota holders and ordinary Icelanders who resent the quota concentration are both anti-EU, but for opposite reasons. The pro-accession camp has not yet made the argument that EU competition law may be the only external mechanism capable of breaking an oligarchy that most Icelanders dislike. That argument, when it surfaces, will reframe the fisheries debate from sovereignty versus access into something altogether more uncomfortable: oligarchy versus democratisation.

The restructuring pressures extend beyond quotas. EU competition law (TFEU Articles 101 and 102) would apply to Iceland’s concentrated seafood market, where a small number of vertically integrated companies control catching, processing, and export. Merger review could constrain further consolidation. State aid rules would scrutinise subsidised harbour fees, fuel tax exemptions, and below-market processing infrastructure. The cumulative effect: an industry constituting 12% of national GDP subjected to regulatory machinery designed for industries that are economically marginal to the member states in which they operate.

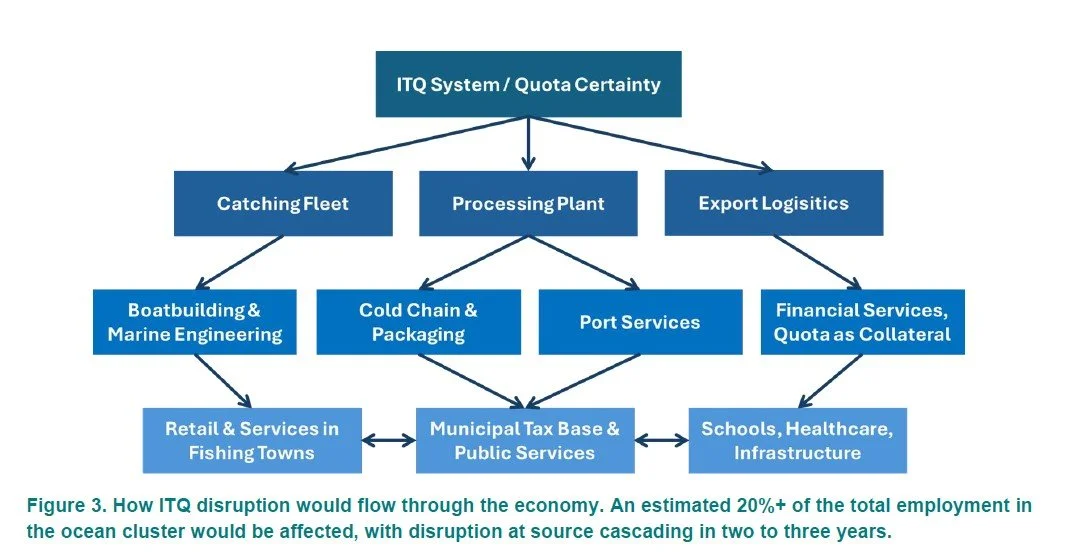

The secondary effects deserve explicit attention. The 12% GDP figure captures direct fishing and primary processing. It does not account for the cascade: boatbuilding and marine engineering whose order books depend on quota certainty; cold-chain logistics built around Icelandic processing volumes; port services; and the financial institutions that have lent against quota assets valued under the current framework. The ITQ system is not merely a fisheries management tool. It is the collateral base for a significant portion of commercial lending. Disruption to quota certainty, whether through CFP reallocation, ownership liberalisation, or competition law challenge, would transmit through the credit system into the broader economy. The fishing towns of the Westfjords and East Iceland are not coastal communities that happen to fish. They are economies in which virtually every job traces back, within one or two links, to the boat.

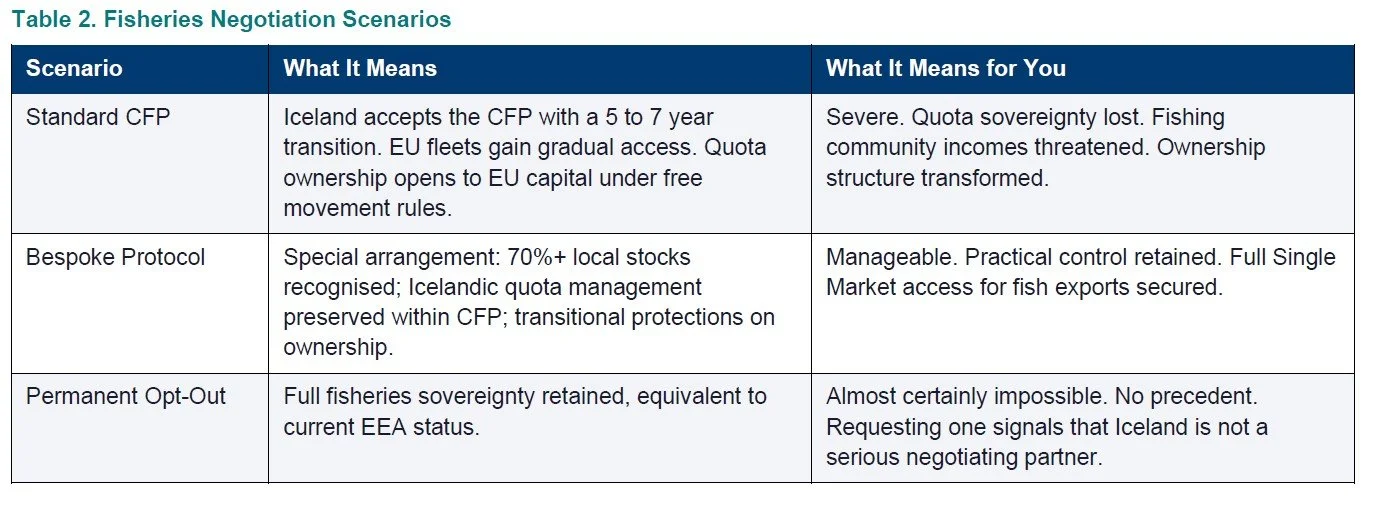

But opening the chapter is not enough. Iceland’s negotiators need to arrive with a fully developed position on four distinct fronts: fleet access, quota allocation baselines, the legal status of quota ownership under free movement of capital, and the compatibility of the ITQ system with EU competition law. Malta’s permanent fisheries protocol, tailored to its specific industry and alterable only with Maltese consent, provides the template. Iceland’s former foreign minister proposed an equivalent ‘Iceland Protocol’ that would preserve EEZ control and block foreign acquisition of quota through company purchases. That proposal never reached formal negotiations. It should be the starting position if talks resume.

Each of these positions is defensible. None will be conceded without something in return. The negotiation is not a petition; it is a trade. Understanding what the Commission and the established fishing member states need from an Icelandic accession (stable North Atlantic stock management, a precedent that does not unravel existing CFP arrangements, access to Icelandic processing expertise) is the prerequisite for constructing a proposal they can accept. The UK’s departure removes the hardest opponent from the table. That advantage is structural but not permanent. The analytical work should be under way before the ballot papers are printed.

4.Borders and Defense

Five years ago, it was possible to argue that NATO provided adequate security guarantees and that EU membership added nothing of strategic value. That argument is now considerably harder to sustain. The security dimension is also, unusually, the one where Iceland’s negotiating position is strongest. A country of 400,000 at the centre of the GIUK gap, with sovereign control over critical North Atlantic maritime space, brings genuine strategic value to the EU’s collective defence posture at precisely the moment when the EU is building autonomous defence capabilities. Arctic geopolitics, the Greenland question, and the collapse of assumptions about transatlantic reliability have made Iceland more strategically valuable to the EU than at any point since the Cold War. That value should be understood and used across the entire accession negotiation, not treated as a separate chapter. Iceland’s geography is a negotiating asset. It should be used as one.

Iceland already participates in Schengen and is associated with the Dublin Convention. EU citizens live and work freely in the country through the EEA. Full membership would formalise arrangements that already exist in practice. Given the tightness of the labour market (unemployment at roughly 3.5%, multiple sectors facing skills shortages), any modest increase in inward migration would more likely fill vacancies than displace workers.

The labour market effects would not distribute evenly. Foreign workers already constitute nearly 24% of Iceland’s employed population, concentrated in construction, tourism, fish processing, and care work. Full membership would not dramatically change the EEA legal framework, but would signal permanence and potentially increase inflows where Icelandic wages exceed continental norms by the widest margins. Care workers, seasonal labour, and lower-skilled construction roles would face the most direct pressure. IT and technical roles, where Iceland already pays below Scandinavian rates, might see less impact. The net effect is likely positive at the aggregate level but negative for specific cohorts in sectors where the wage premium is largest.

The security dimension is where the ground has shifted most dramatically. Iceland has no standing military. Its defence rests on NATO and a bilateral agreement with a United States that has imposed tariffs on Icelandic goods, suggested through its ambassador-nominee that Iceland become the '52nd US state,' and made overt moves toward acquiring Greenland. Greenland's own prime minister has urged citizens to prepare for the possibility of an American invasion. Russian naval activity in the North Atlantic continues to increase.

The EU is not a military alliance and membership would not replace NATO. But it would provide a complementary framework. The mutual defence clause in TEU Article 42(7) establishes a binding obligation of aid and assistance if a member state is the victim of armed aggression.18 The Common Foreign and Security Policy, PESCO, and the European Defence Fund provide collective options that no bilateral relationship can replicate. For a country of 400,000 sitting at the centre of the GIUK gap, the ability to respond to external pressure as part of a community of 450 million is a material change in strategic position.

5.Energy: the issue not being discussed

The fisheries derogation has a template: the CFP permits transitional arrangements and special management areas. The energy derogation has none. No EU accession candidate has ever operated an energy system like Iceland’s, because no candidate has ever used below-market renewable energy as the foundation for domestic value-added industries at this scale. That means Iceland would be writing the template, not following one. It is a harder negotiation, but not an impossible one. The EU has its own strategic interest in Icelandic renewable energy: carbon-neutral power for European AI and data infrastructure, geothermal expertise applicable across the continent, and a demonstration case for 100% renewable industrial economies. A negotiating team that understands what the EU wants from Icelandic energy (not just what it demands under the acquis) has material to work with. Discovering this problem after the talks have started would be a strategic failure of the first order. Mapping the negotiating space before they begin is the minimum requirement.

The received wisdom holds that fisheries is the decisive issue in Iceland's EU debate. Within twelve months of a yes vote, energy will have overtaken it.

Iceland generates nearly 100% of its electricity from renewable sources: roughly 70% hydro and 30% geothermal. The state-owned National Power Company, Landsvirkjun, produces approximately 71% of all electricity and sells the bulk of it to energy-intensive industrial customers through long-term Power Purchase Agreements at prices well below European wholesale levels.19 Energy-intensive industry consumes 80% of total electricity production. These below-market PPAs are the foundation of Iceland's industrial strategy. They are the reason Alcoa operates a 346,000-tonne aluminium smelter near Reydarfjördur. They are the reason data centre operators locate in Iceland, where one company recently reported an 84% cost saving over equivalent UK facilities.

The data centre sector now accounts for over 5% of Iceland's GDP and is growing faster than any other segment of the economy. AI infrastructure demand from European companies seeking carbon-neutral computing is accelerating the buildout. According to government estimates, effective AI adoption could add between USD 1.4 billion and USD 11.8 billion to Iceland's economy by 2029. The sector has shifted from cryptocurrency mining to high-value AI workloads, creating technical jobs and attracting international investment. Iceland's data centre market is projected to reach USD 812 million by 2030, growing at a compound rate of over 11% annually.

Before examining the regulatory collision, there is a question worth asking: could Iceland sell surplus power to Europe? The price gap between Icelandic and European wholesale electricity is enormous. Studies of a proposed HVDC submarine cable to the UK have estimated export revenues in the hundreds of millions of euros annually. The problem is that the opportunity and the risk are the same cable. An interconnector that enables export at European prices also enables European price signals to reach Iceland. Market coupling rules under Regulation 2019/943 would pull Icelandic wholesale prices toward the European level, which is precisely the mechanism that would destroy the below-market PPA model. Iceland could earn export revenue from surplus generation while losing the industrial base that consumes 80% of current production. The energy opportunity exists in theory. In practice, it is inseparable from the energy risk.

The Regulatory Collision

This model is structurally incompatible with EU internal energy market rules. The Third Energy Package (Directive 2009/72/EC) and the Clean Energy Package (Regulation 2019/943) require unbundling of generation from transmission, non-discriminatory third-party grid access, and market-based pricing.22 Landsvirkjun's below-market industrial PPAs could be classified as prohibited state aid under TFEU Article 107, because they grant specific undertakings an economic advantage through state resources at rates below what the market would otherwise provide.

Under the EEA, Iceland is protected. Because its grid is physically isolated from the European mainland with no interconnector, the European Commission confirmed in 2019 that the Third Energy Package 'affects in no way the Government of Iceland's full sovereign control over Iceland's energy resources. Full EU membership would remove that protection. Iceland would become subject to the complete energy acquis, and the legal basis for the current PPA model would disappear.

The Volatility Trap

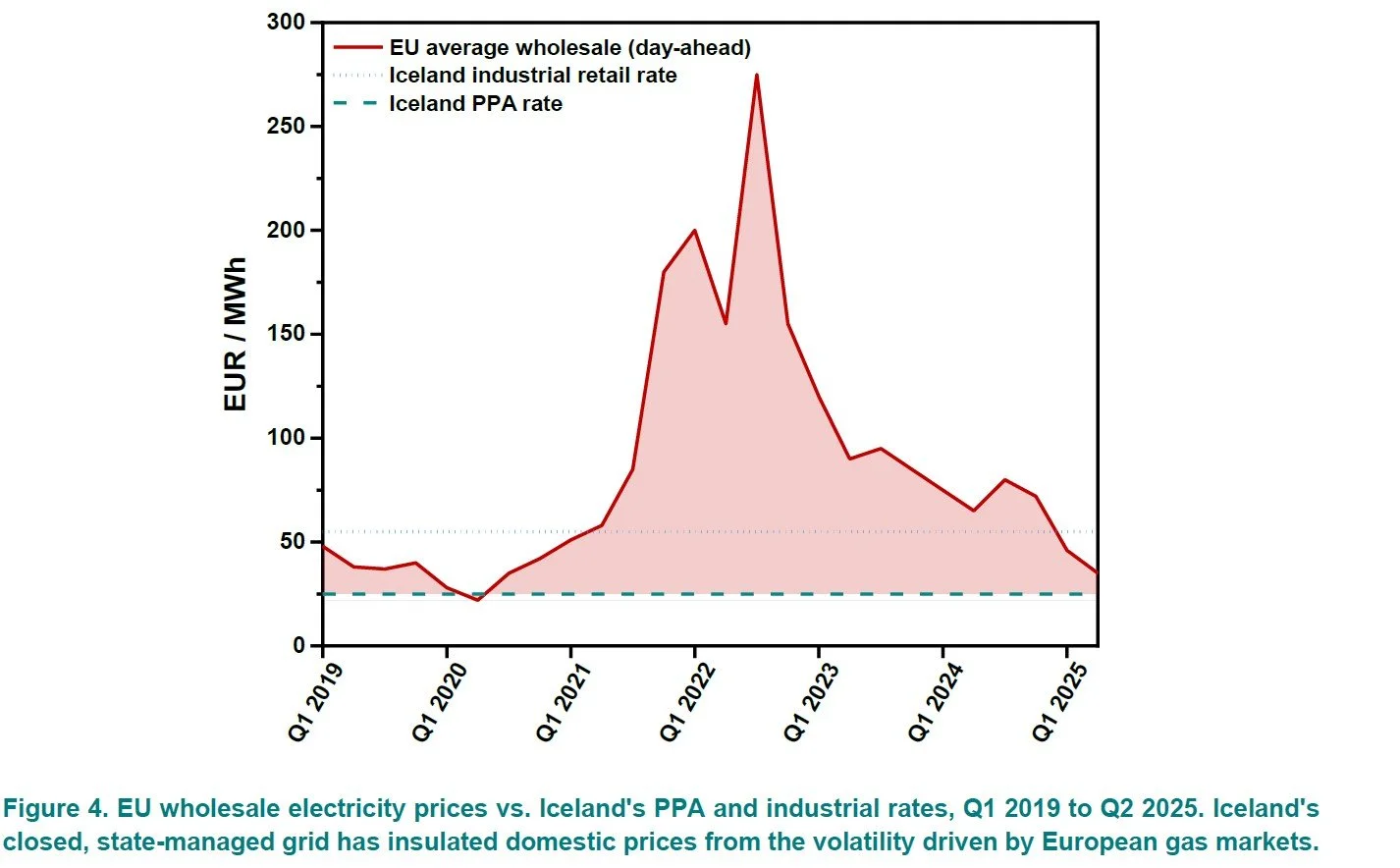

There is a further dimension that has received no attention at all. Iceland's 100% renewable electricity system has, to date, insulated Icelandic consumers and industry from the fossil fuel price volatility that has battered the rest of Europe. EU wholesale electricity prices averaged approximately USD 90/MWh in the first half of 2025, around 30% higher than the same period in 2024, driven in large part by elevated natural gas prices. Price spikes above EUR 150/MWh occurred in 9.3% of hours in 2025. The ACER monitoring report found that EU wholesale prices remain higher and more volatile than pre-crisis levels

EU internal energy market rules, if applied to Iceland through full membership and eventual grid interconnection, would expose Icelandic electricity prices to this volatility for the first time. Even without a physical cable to the mainland, market coupling regulations and third-party access requirements could pull Icelandic wholesale prices toward European levels. Icelandic electricity currently costs roughly USD 0.066 per kWh for industrial users. European wholesale prices have averaged EUR 35 to 90/MWh in recent quarters, depending on the period. The gap between these figures is the entire competitive advantage on which Iceland's aluminium and data centre industries are built.

EU internal energy market rules, if applied through full membership, would expose Icelandic prices to this volatility for the first time. Even if Icelandic prices remained somewhat lower than the European average, the introduction of market-based pricing mechanisms would expose the country to the oil-and-gas-related price swings from which it has been largely insulated. The IEA has documented how European gas market volatility transmits directly into electricity prices, with gas-fired generation setting the marginal price in competitive wholesale markets. Iceland's closed, state-managed, renewables-only grid currently avoids this transmission entirely. EU membership would end that insulation.

The investment implications follow directly. Data centre operators locate in Iceland for three reasons: 100% renewable power, political stability, and electricity prices far below European wholesale levels. If EU energy market rules eliminate the third, the business case weakens substantially. State aid scrutiny of Landsvirkjun’s below-market PPAs would create regulatory uncertainty before any formal reclassification. The mere opening of an EU energy chapter, if it signals that the PPA model is legally vulnerable, could freeze investment decisions during the multi-year negotiation period. The aluminium smelters, with decades-long PPA commitments, are somewhat insulated. The data centre sector, where investment horizons are shorter and location decisions more mobile, is not.

Conclusion

Through the EEA, Iceland has already incorporated over 10,000 EU legal acts into its domestic framework. It accepts free movement of persons, goods, services, and capital. It contributes to EU cohesion funds. It implements EU directives across the full breadth of Single Market regulation. In functional terms, Iceland is a member of the European Union in every domain except the ones that matter most to the domestic debate: agriculture, fisheries, energy, and monetary policy.

The balance of evidence in this assessment suggests that full membership would deliver a net positive for the average Icelander, driven principally by monetary stabilisation, the elimination of indexed mortgage debt, and enhanced collective security. That conclusion is real but conditional. It rests entirely on the assumption that accession negotiations produce workable arrangements on fisheries, energy, and the conversion rate. If they do not, the political economy of the entire process collapses, as the 2010 to 2013 experience demonstrated.

This assessment has identified issues in each dimension that have received insufficient public attention: the interaction between indexed mortgages and euro adoption; the conversion rate as a one-time wealth transfer mechanism whose outcome depends on political negotiation, not economic optimality; the vulnerability of the ITQ ownership structure to EU capital mobility and competition law; the cascade through secondary industries that depend on quota certainty; and the incompatibility between Iceland’s state-managed PPA model and EU internal energy market rules. Each of these issues is navigable. None of them will navigate themselves.

The difference between a good outcome and a bad one will not be determined by whether Iceland votes yes or no on 29 August. It will be determined by what happens the day after a yes vote: whether the government has a negotiating team in place that understands not only Iceland’s interests but the institutional incentives of the Commission, the Council, and the established member states; whether that team has mapped the negotiating space on each chapter before the talks begin; and whether it arrives with proposals that the EU can accept without setting precedents it cannot sustain.

The 2010 to 2013 negotiations were derailed not by an abstract conflict over sovereignty but by a specific bilateral mackerel dispute that gave two member states veto power over the fisheries chapter. Iceland was saved from a full trade embargo only by relationships its foreign minister had personally cultivated with the Swedish and German foreign ministers. The lesson is not that negotiation is futile. It is that negotiation at this level requires institutional knowledge, bilateral relationships, and a granular understanding of what each counterparty needs in order to say yes. Iceland’s strategic assets (its geography, its renewable energy, its fisheries management expertise, its North Atlantic position) are genuine and significant. They are also perishable: they have value only if deployed by negotiators who understand the room.

For the undecided voters who will determine the outcome, the question is not whether EU membership is good or bad for Iceland. It is whether Iceland is prepared to negotiate membership well. On the evidence available, that preparation has not yet begun. It should.